Institutional Insights: Goldman Sachs Q2 Earnings Playbook

Expect a Strong 1Q, with Results Likely Above Consensus: Earnings season unofficially begins next week with the major banks. Our economists estimate 1Q26 real U.S. GDP growth at 3%, a pace historically associated with double-digit EPS growth. Against that backdrop, we believe the market’s already elevated expectation of 12% YoY EPS growth—the highest since 2021—can still be exceeded. If so, this would mark the sixth straight quarter of double-digit earnings growth, the longest streak since the Global Financial Crisis.

Caveat on Market Reaction: Despite what should be a solid quarter fundamentally, we expect the market response to earnings to be more muted than usual. This remains a macro-driven tape rather than a micro-driven one, which typically means less upside for earnings beats and lower volatility around individual reports. The setup resembles Q1 2025 during the tariff shock, when company-specific results mattered less than the broader macro backdrop.

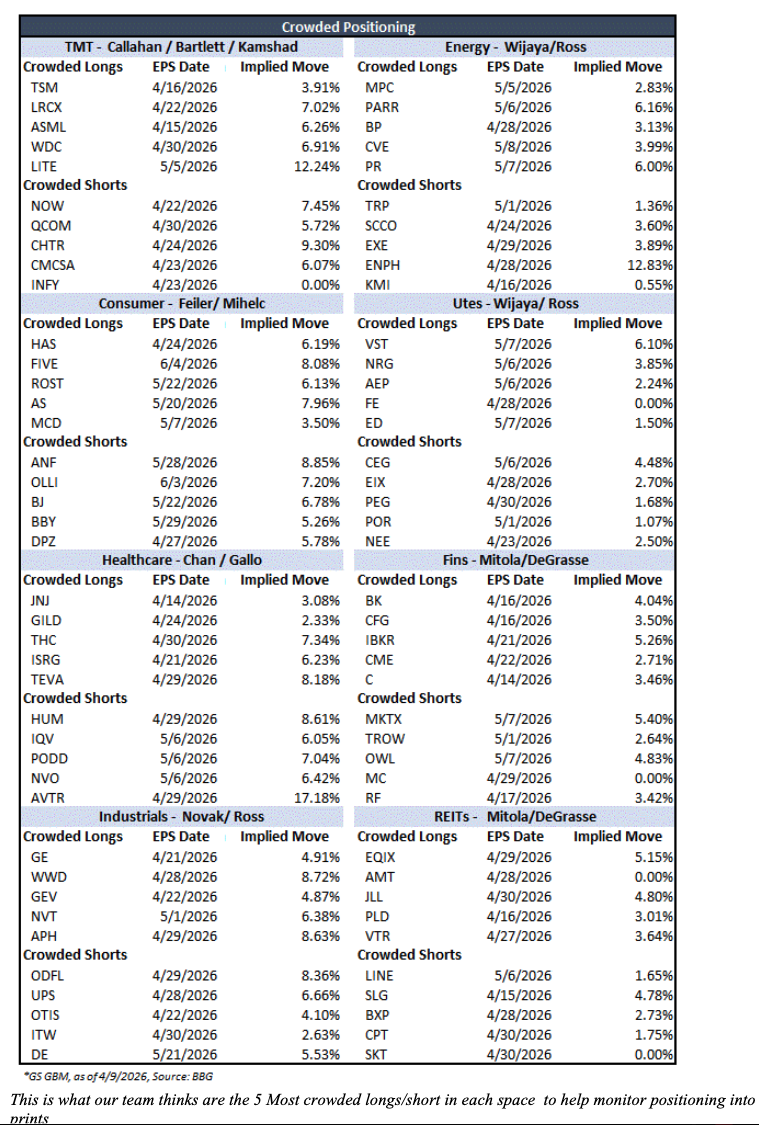

Where Capital Could Be Redeployed: If earnings come in strong and geopolitical tensions do not escalate further, the key question is where investors put money back to work. A favorable setup could drive renewed interest in high-conviction longs, particularly AI beneficiaries if management teams continue to highlight adoption trends. In that scenario, we could see re-engagement in the names that outperformed during the recent ceasefire rally—momentum longs, AI winners, memory, semis, and related growth areas. Positioning is also cleaner than it has been, which raises the possibility that stock reactions could be better than many expect.

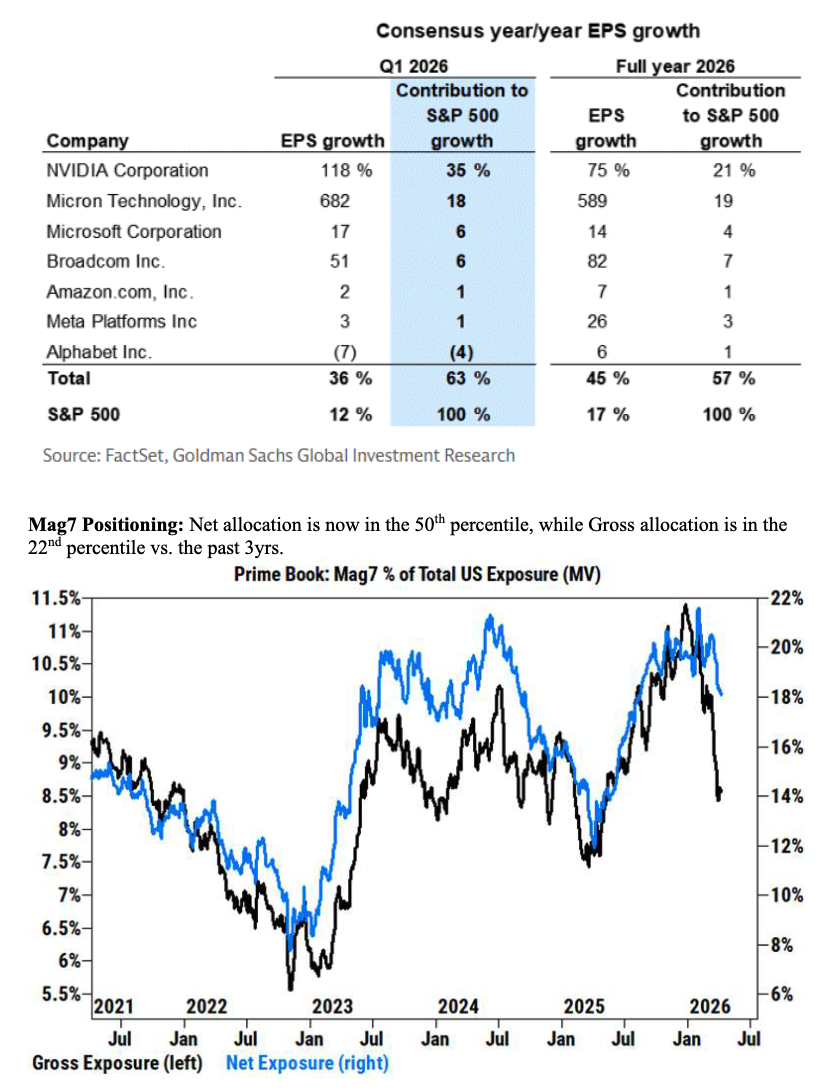

Cleanest Setup of the Year for the Mag 7: Within the Mega Cap tech complex, positioning looks as clean as it has all year. Net exposure sits around the 50th percentile, while gross exposure is in just the 22nd percentile versus the past three years. We have also seen increasing client interest in this group over the last week. Any credible evidence of AI return on investment could be a major catalyst. Recent comments from Amazon CEO Andy Jassy, which highlighted both AI momentum and improving visibility into returns on invested capital, reinforce that optimism.

Key Tailwinds: AI investment remains the primary engine of earnings growth, accounting for roughly 40% of total S&P 500 EPS growth this year. Information Technology alone is expected to deliver 44% EPS growth, representing 87% of total earnings growth in Q1. AI-related tailwinds have strengthened further in recent weeks, especially after Micron guided next-quarter EPS roughly 60% above consensus.

Key Headwinds: There are still risks to watch. Higher oil prices and recent U.S. dollar strength could limit the size of earnings beats versus prior quarters. We are also monitoring whether rising energy costs and supply chain disruptions begin to pressure corporate profitability. That said, this appears more likely to become a bigger issue in 2Q through 4Q than in the current quarter. Net profit margins reached a record high in Q4 2025, but input cost pressures had already begun building even before the latest conflict.

Iran and the Wide Range of Outcomes: History suggests that the range of outcomes following oil shocks is wide. Over the 12 months after past energy disruptions, S&P 500 EPS growth has ranged from -15% following Iraq’s invasion of Kuwait in 1990 to +18% after the start of the Second Gulf War in 2003. In both cases, Consumer Discretionary and Energy were among the most affected sectors. Importantly, EPS is not especially sensitive to oil prices on its own. The bigger risk is a prolonged disruption severe enough to slow GDP growth materially.

Consumer Remains Resilient: One of the biggest debates in recent weeks has been whether the consumer can absorb higher gasoline prices without weakening. So far, the consistent message from corporates, high-frequency data, and early earnings reads is that the consumer has remained resilient, with notable strength in March. We expect a solid earnings season for consumer-facing companies, excluding housing and packaged food, despite the weakest University of Michigan sentiment reading in roughly 75 years.

A Throwaway Quarter? The prevailing view is that guidance and management commentary may matter more than reported results this season. Investors are likely to hear a lot of “wait and see” language from companies, with management teams citing macro uncertainty and delaying more definitive outlooks. That could limit the market impact of even strong prints, especially if companies choose to blame the macro environment and defer visibility to later quarters.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!